What did the future of software look like in 1984? That year, the U.S. Department of Commerce commissioned a report to analyze the future of the software industry in the U.S. and abroad. The industry was booming, led by U.S. players, but many feared increasing international competition.

Other than its explosive growth, the software industry of 1984 looked shockingly different from today’s. Except for IBM, none of the top 20 companies globally by revenue then are leading tech players today. Microsoft was mentioned in the 1984 report only to note that it was not publicly traded and thus did not release financials. The key players—NCR originally stood for “National Cash Register”—are almost unrecognizable to a modern reader.

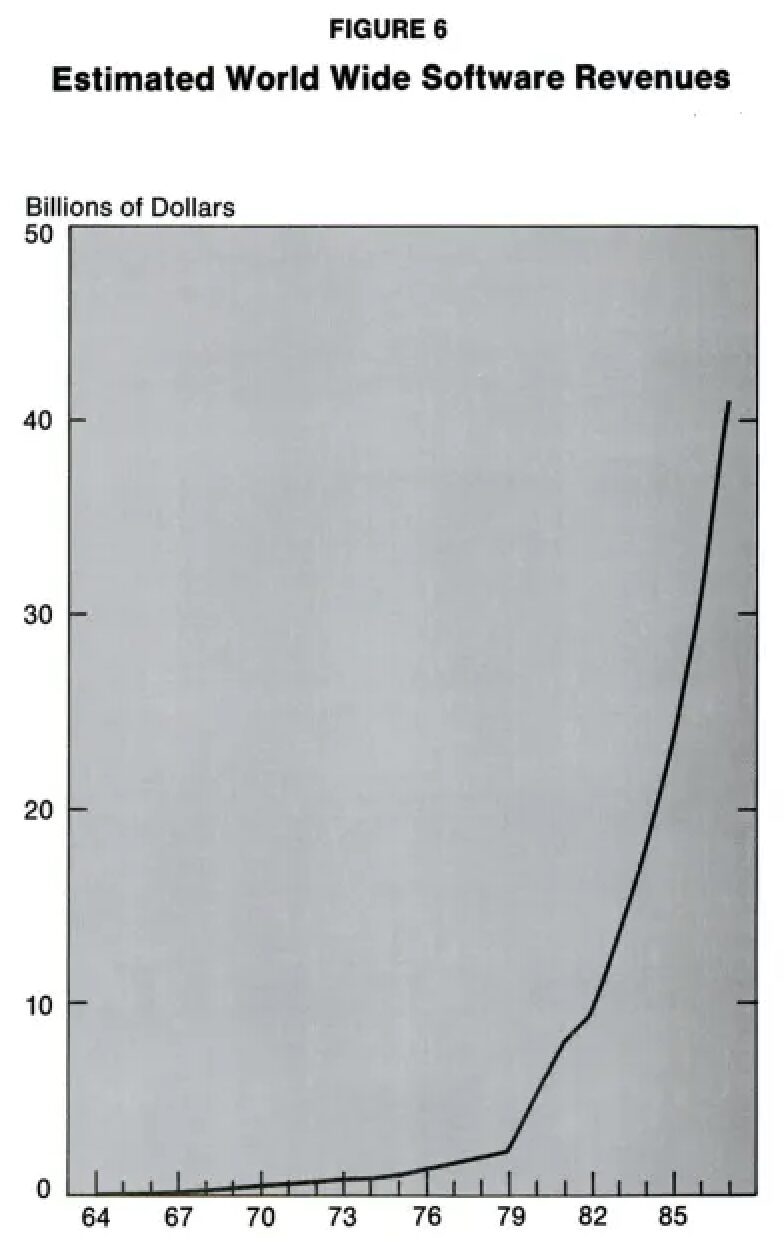

That’s because the industry’s explosive revenue growth (see below) was being driven by a major business model shift. The leading players of 1984 were losing ground to new upstarts. Before the late 1970s, software was largely provided for a specific company to enable its unique computing needs. Its business model was like consulting—hence the presence of Arthur Andersen and Japan Business Consultants on the list. Software consultants would write specific programs to manage airline reservations or banking transactions. They’d sell them to one, or at most a handful, of companies. The revenue would cover the costs of a well-paid professional workforce, plus some margin on top.

This model was beginning to be replaced by “packaged software”—the provision of off-the-shelf products for a wide range of customers. The rise of minicomputers and later personal computers were creating a broad base of computer users who wanted software. Rapid improvement in computing power let even basic machines run more complex software packages. Programs like Visicalc—the first major spreadsheet program for financial analysis—could be used by anyone with a PC and a need for financial modeling. The market was growing fast, even though in the early 80s packaged software still represented a minority of U.S. software employment.

Then as now, the software industry had high R&D expenditures—four times the average across industries as a share of revenue, according to the report. Profit margins were twice the S&P average. Then as now, a small number of big firms earned most of the industry’s revenue. The shift to packaged software raised the prospect of adding customers at zero marginal cost. Excluding sales and marketing, the marginal cost of providing a new Visicalc package was only the floppy disk the program was delivered on. Only near-monopolies like Microsoft would benefit from such low customer acquisition costs. Even still, the whole package software industry benefited from a model that did not require the number of highly paid software engineers to scale linearly with the number of users of the software.

What was the status of the software industry outside the U.S.? Very small and poorly positioned in packaged software:

The U.S. software industry held an estimated 70 percent of an estimated 1983 world market of $18 billion and its revenues were ten times larger than those of either France or Japan, its nearest competitors. More than half of its worldwide revenues came from packaged software, while most of the leading foreign suppliers gained the bulk of their revenues from custom software.

What explained the strong U.S. position? The report argued:

(1) Long term leadership of U.S. hardware manufacturers in the world’s computer systems markets through their technological, management, and marketing progress;

(2) the industry’s’ innovative and entrepreneurial character; and

(3) the size, sophistication, and homogeneity of the U.S. market.

…

Because of the interdependence of hardware and software, the U.S. competitive advantage in computer equipment has contributed significantly to the U.S. competitive advantage in software during the early stages of the industry’s growth.

U.S. manufactured computer equipment has historically represented a major share of the installed base of such equipment worldwide. Approximately 80-85% of all computers in use worldwide has been supplied by U.S. firms. This has provided U.S. software developers…with distinct competitive advantages….not only from the close interdependence between equipment and software, but also from the economics achievable in distribution, marketing and after-sales support.

The advantages to the U.S. software industry of U.S. leadership in the equipment sector are clearly evident in the personal computer sector. U.S. industry has led in microprocessor technology, a critical component in the personal computer, first developed in the United States. U.S. software firms, in turn, have developed operating systems for these computers which have become de facto standards worldwide.

That last paragraph perfectly describes Microsoft’s origins. It really helps to have a full tech stack, as Silicon Valley might put it. Ecosystem effects really matter, as an economist or sociologist might rephrase it. Or, in the language of China’s leaders, having a “complete industrial system” is a major competitive advantage

What about the world’s other important software players? One, interestingly, was France, which “was the leading software supplier in Europe and second in the world.” Yet it was focused less on packaged software than the U.S., leaving it less well positioned. A second competitor was Japan. On top of winning market share in traditional industries from steel to autos, the Japanese were, in 1984, crushing the U.S. semiconductor industry, especially in memory chips. So it was reasonable to ask whether Japan might win in software, too.

U.S. programmers were “creative” but “lacking in discipline” and therefore error prone, the report found. It cited a source that Japanese programmers could produce 6x the code of American programmers with a tenth the bugs. But the report also praised the “efficiency of U.S. software managers.” It’s on face a puzzling claim: was U.S. management really more efficient if their employees were doing less work with more errors? But software output has never been best measured in lines of code.

In the United States, software developers are typically seen as creative and individualistic, but generally lacking in discipline. By contrast, the Japanese programmers appear more disciplined, group oriented, and obsessed with quality.

Some observers claim these differences account for higher software development productivity and fewer programmer errors in Japan. One report, for example, claimed that Japanese programmers average 2000 lines of code per month (versus less than 300 lines per month for U.S. programmers) and have one-tenth the error rate (”bugs”) of their U.S. counterparts. However, some observers claim these productivity differences are counterbalanced at the software project level due to the superior efficiency of U.S. software managers.

Despite low error rates, “Japan is far behind the United States in basic research and advanced development of software, and does not appear to be catching up.” It has “never developed a programming language or an operating system that has become a de facto standard internationally. It was very good at video games and process control, but not for “standard applications packages for business use.” And—as the rise of Microsoft would soon show—that’s where the money was.

Professor Chris Miller is a geopolitical expert who talks about the origin, impact, and future of AI. He is the author of Chip War: The Fight for the World’s Most Critical Technology, a book that explains how computer chips have made the modern world—and how the U.S. and China are struggling for control over this fundamental technology. Chip War won Financial Times’Best Business Book of the Year award. Breaking down the motives behind international politics and economics in a thoughtful and concise manner, Miller provides audiences with fresh, alternative perspectives and leaves them wanting to know more. Contact WWSG to host him at your next event.

This is an Op-ed by WWSG exclusive thought leader, Dr. Scott Gottlieb. Many consumers and medical providers are turning to chatbots, powered by large language…

This piece is by WWSG exclusive thought leader, Sara Fischer. Amid the craziest news cycle in recent memory, AI-generated deepfakes have yet to become the huge truth…

Written by WWSG exclusive thought leader, Evan Feigenbaum. In mid-July, China concluded a pivotal economic strategy meeting, where it quadrupled down on technology as the…