Dr. Sanjay Gupta: A New Way to Heal

Doctors have long prescribed pills and procedures. But for some people, that isn’t enough. Sanjay sits down with Julia Hotz, author of The Connection Cure, to explore the…

Thought Leader: Sanjay Gupta

Sheila Bair is former FDIC chair and senior fellow, Center for Financial Stability.

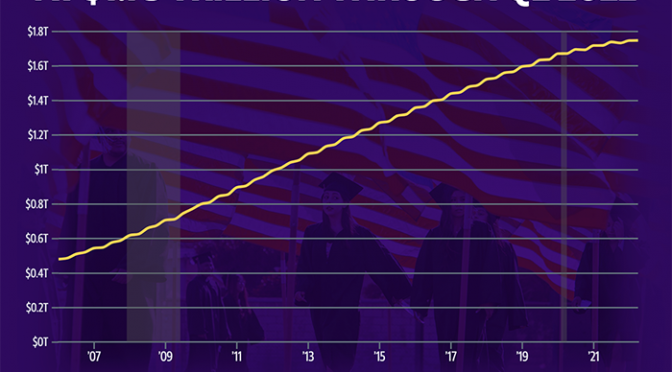

President Biden has finally made a decision about student debt cancellation, going significantly beyond the $10,000 in forgiveness that he embraced as a presidential candidate. Of the 43 million borrowers eligible for his plan, 27 million Pell grant recipients will qualify for $20,000 of relief, with the remainder qualifying for $10,000. Conservative estimates put the cost at about a half trillion dollars.

But most problematic is the plan’s complete lack of meaningful reforms to address the complexity and moral hazard that have long plagued the federal student loan system. Without those reforms, the Biden plan will likely make the system worse. According to one estimate, in just five years, total student debt will be right back to $1.6 trillion, where it is now.

I have previously written in support of $10,000 in debt cancellation. I have compassion for the many students struggling to repay their loans, particularly low-income, first generation students. The government has been culpable in a system where 40% of borrowers are unable to pay down just $1 of their debt within three years of graduation. It has failed to impose meaningful disclosure obligations on colleges or responsibility for some portion of losses when their students are unable to repay. Debt cancellation, without reform, simply doubles down on this lack of transparency and accountability. Emboldened by the prospect of future debt forgiveness, colleges with no skin in the game will keep encouraging students to borrow to the max, and students, who are given little, if any information, about the affordability of their loans, will continue to do so. Tuition and other costs will continue to rise, fueled by easy access to federal loans proceeds and leading to even more borrowing.

To stop this cycle, we must have better transparency, common sense caps on borrowing, risk sharing for colleges, and disqualification of schools with consistently poor student outcomes. Unfortunately, while the Biden plan gives lip service to college accountability, its only new initiatives are to publish a watch list of programs with the high debt levels and require “institutional improvement plans” from the worst college actors. This treats moral hazard and rent seeking as a narrow problem confined to specific programs or institutions, when in fact it is systemic throughout higher education finance.

Hyper-complexity has also plagued the system, offering an array of multiple loan types and repayment options. This complexity has added to the confusion and opacity around student borrowing. Unfortunately, the Biden plan adds to complexity by creating yet another income-based repayment option and more avenues for debt forgiveness for borrowers with small loans and those in public service. While these may have individual merit, layering them on top of the many repayment plans already available will only add to borrower confusion.

The fiscal implications of the plan are also troubling. At a cost of half a trillion dollars, it is double the estimated $250 billion price tag of the president’s original $10,000 debt cancellation plan and wipes out the $305 billion in budget savings contained in the recent Inflation Reduction Act. Not that deficit-financed spending programs are anything new in the nation’s capital, but this is being done without Congressional approval and at a time when inflationary pressures demand curbs on government largesse.

Proponents of the program argue the plan will not be inflationary because it is combined with the resumption of loan payments at the beginning of next year. (Student borrowers have been enjoying a payment pause since March 2020, first instituted by President Trump in response to the pandemic.) This, they say, will negatively impact household spending, offsetting any inflationary impact from debt cancellation. But $20,000 in debt forgiveness will also create significant new capacity to take on more debt, particularly mortgage loans, where high student debt burdens have disqualified many potential homeowners. It’s no surprise that the head of the National Housing Conference was one of the first business leaders to support the program. Ordinarily, I would say increased homeownership opportunities are a good thing, but the residential housing market has been running red hot for nearly three years. Rising home prices have been a key driver of inflation, increasing by about 20% in both 2020 and 2021, and continuing at a 10% pace this year. The last thing we need right now is more demand.

Of course, the Biden Administration’s arguments against inflationary impact assume that payments will in fact resume next year. But borrowers have become accustomed to not making loan payments. Will they truly be prepared in four months? The Department of Education and its loan servicers will have to work hard to convince them that this time they mean it, given past false signals that payments will resume. And if we are in a recession, the political pressure to pause again may well be irresistible to the Democrats and their core base.

A final concern is the weak legal basis underpinning the program. The administration is relying on a provision of law passed in the wake of the 9/11 terrorist attacks that gives it authority to provide broad relief in a national emergency to help borrowers who are “in a worse position financially” because of the emergency. It will be hard to demonstrate that the 43 million borrowers potentially benefiting from debt cancellation are all in a “worse position financially” because of the pandemic. Some legal scholars have argued that no one has standing to challenge the program, but I think there is a good chance that our increasingly conservative judiciary will find a way to review the program and invalidate it as exceeding the bounds of the president’s authority. Thus, the plan’s sweeping debt cancellation may never happen at all.

I voted for President Biden in 2020 — the first time I ever voted for a Democrat in a presidential election. I want him to succeed. Sticking to his plan of $10,000 in forgiveness and limiting it to Pell recipients would have been less expensive, less controversial, less inflationary, and much easier to administer. It would have also stood a better chance of withstanding legal challenge. It’s not too late for his administration to correct course by working with Congress on a meaningful package of reforms that will simplify the system, address moral hazard, and authorize some level of debt cancellation. This would give past borrowers legally certain relief and future borrowers a system that is truly aligned to serve their best interests.

Dr. Sanjay Gupta: A New Way to Heal

Doctors have long prescribed pills and procedures. But for some people, that isn’t enough. Sanjay sits down with Julia Hotz, author of The Connection Cure, to explore the…

Thought Leader: Sanjay Gupta

Niall Ferguson: Trump’s World Order Live From Davos

Live from Davos, Scott Galloway and historian Niall Ferguson examine why today’s geopolitical moment looks less like a “new world order” and more like a…

Thought Leader: Niall Ferguson

Mike Pence Talks Trump’s Foreign Policy

Former US VP Mike Pence discusses President Trump’s foreign policy with Greenland, Russia, and Ukraine. He says he commends President Trump on finding a framework…

Thought Leader: Mike Pence