By Chris Miller & Joris Teer | As tensions with China grow, Western countries need to do more to finance and build alternative supply chains for critical minerals.

As tensions between China and its major trading partners escalate, Beijing has a powerful card to play — its near monopoly on the mining and processing of a wide variety of critical minerals.

Weaponizing trade in the materials that advanced industries require could have immense economic consequences. And to address this, Western countries need to do more to finance and build alternative supply chains for critical minerals.

The recently announced EU investigation into Chinese subsidies for electric vehicles (EV) illustrates the country’s powerful role in critical mineral value chains. When it comes EVs, China controls much of the value chain — from mining to refining, to processing, to battery-making, to manufacturing vehicles. Even EVs manufactured abroad usually require minerals refined in China or by Chinese companies. And as mineral demand increases due to the energy transition, Beijing’s leverage is only growing.

So, could China use its market position in critical minerals as a coercive tool?

China’s market position creates extraordinary risks. Minerals aren’t just central to the green transition and digitalization, they are essential building blocks throughout vital sectors.

Take rare earths, for example, a group of 17 minerals used to manufacture devices such as pacemakers, MRI machines, drones, fighter jets, wind turbines and hard drives. China possesses 90 percent of the world’s refining capacity for rare earth elements critical for the high-powered permanent magnets needed in everything from EVs to iPhones.

Or consider cobalt, which is a critical mineral for many battery technologies. Two-thirds of the world’s cobalt is mined in the Democratic Republic of Congo, but these mines are predominantly Beijing-owned and refining often takes place in China.

Beijing also has a strong position in materials like gallium and germanium, which are used to manufacture respirators, defibrillators and electric engines, as well as electronics. It produces 97 percent of the world’s gallium and 68 percent of its germanium.

Russia’s manipulation of gas markets in 2022 has demonstrated that supposedly mutually beneficial interdependence is far from a guarantee of trade peace. Disruptions in mineral supply could cause even more harm.

But while Western policymakers have identified critical minerals trade as a risk, progress in addressing these dependencies has been limited, with the European Union lagging Japan and the United States.

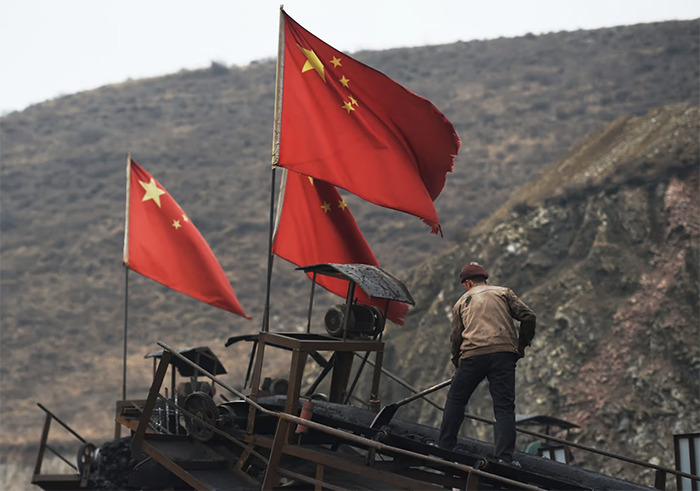

Minerals aren’t just central to the green transition and digitalization, they are essential building blocks throughout vital sectors | Gohchai Hin/AFP via Getty Images

The challenge is that private firms naturally buy the cheapest minerals available, and China’s monopolistic position lets it set prices for some materials to guarantee competitors in market economies can’t create viable businesses. Whenever it looks like a competitor is winning market share, China can flood the market, cutting prices. There is no world antitrust agency to take on China’s market power.

China’s advantages aren’t geological, they’re political. Chinese firms benefit from cheap loans from state-owned banks; lax environmental standards mean cheaper production; and Beijing’s state-owned enterprises have scoured the world for decades to lock up mining concessions.

However, the West does have options. The green energy transition and digitalization create new demand that could be channeled to support mining and refining in trusted countries. Yet, whether this new supply emerges hinges on whether governments create the policy conditions to make other suppliers of critical materials financially viable.

The Japanese and U.S. governments have supported the search for alternative supply sources. For example, the Japan Organization for Metals and Energy Security has invested in the Australian firm Lynas to ensure a large share of Japan’s rare earth needs are met.

Meanwhile, in the U.S., the Inflation Reduction Act counters Beijing’s advantages in the EV value chain, making companies that use either components or materials from “foreign entities of concern” — like Russia or China — ineligible for tax credits.

And by reopening the Mountain Pass Mine in California, the U.S. has climbed back from zero percent of global rare earth mining only 12 years ago to 16 percent in 2020, supported by a Pentagon program to guarantee defense production. In addition to bringing online domestic mining, U.S. President Joe Biden’s recent visit to Hanoi and signing of an agreement to facilitate investment in Vietnam’s rare earth reserves underlines the seriousness with which U.S. diplomacy approaches achieving greater mineral security. Vietnam sits on the second-largest known deposit of rare earths and intends to break into China’s refining and magnet-making monopoly too.

The EU has yet to achieve any comparable successes. It is in the process of setting up a permanent magnet-making facility in Estonia, however. And the bloc can do more to leverage its leading role in the energy transition.

For example, the North Sea nations’ investment in offshore wind creates plentiful demand for rare-earth-based permanent magnets that are used in wind turbines. But while this could be used to spark mining, refining and magnet production in trusted countries, governments have generally ignored geopolitical risk in designing tenders, so these investments have intensified reliance on rare earth magnets made in China.

Advanced economies need to do more to counter Beijing’s monopolistic position in upstream materials value chains. In addition to the announced EU probe into Chinese EV subsidies, they should commission formal studies to understand and address market distortion in the entire value chain of all China-mined or -refined critical raw materials.

Along these lines, the EU Critical Raw Materials Act calls on member countries to set up raw material observatories to track dependencies. This is a good first step.

But advanced economies — and especially the EU — need better mechanisms for bringing new supply online. Opening new mines and refineries in democracies is difficult due to extensive consultation processes and “not-in-my-backyard” sentiments. Receiving construction permits for such projects can take years. Government financing — like the Pentagon’s support for rare earths mining — may be needed to overcome China’s non-market price advantages.

Bringing new sources of supply from trusted partner countries online is the only way to address China’s choke hold. Action is needed immediately because according to one estimate, it takes between 7 and 20 years to open a new mining facility.

The alternative is to let China consolidate advantages in a sphere where it has escalation dominance, at a time when escalation looks increasingly likely.

Is there a deeper strategy underlying President Trump’s actions? Dan is joined by historian, Free Press columnist, CBS contributor, and Senior Fellow at Hoover Institution…

Loretta Mester, Fmr. Cleveland Fed President, joins ‘Closing Bell Overtime’ with reaction to Pres. Trump’s announcement of Kevin Warsh as his nominee for the next…

We all know we should brush and floss our teeth. But the reason goes beyond a sparkling smile and keeping bad breath at bay. The mouth is a critical and often overlooked organ when it comes to improving overall health. Dr. Sanjay Gupta sits down…