Dr. Scott Gottlieb on Finding Cures for Rare Diseases

Former FDA Commissioner Dr. Scott Gottlieb joins ‘Squawk Box’ to discuss the ongoing research and efforts at the FDA to find cures for rare diseases.…

Thought Leader: Scott Gottlieb

The Ukraine crisis may yet produce the biggest war in Europe since 1945. Or it may produce some strange new hybrid of cyberattacks, “little green men” and maskirovka (military deception) that won’t quite match our preconceived notion of war. Or — though this now seems the lowest-probability scenario — President Vladimir Putin may turn out to be Russia’s answer to “The Grand Old Duke of York,” who (as well-educated children know) “had ten thousand men / He marched them up to the top of the hill / And he marched them down again.”

In January, I warned: “War is coming.” Yet history is full of wars that nearly happened but then didn’t, from the Franco-German “War in Sight” crisis of 1875 to the Cuban Missile Crisis of 1962. For regular investors, these are nail-biting times because wars, unless they are very small and asymmetrical, tend to have big financial consequences. For speculators, by contrast, war scares are golden opportunities. Position yourself correctly, and you can make a killing if the dogs of war are unleashed — though if the hellhounds get sent back to their kennels, it’s you who gets killed and the guy who bet on peace gets the champagne.

In normal times, markets ebb and flow on the latest economic statistics. During a war scare, by contrast, it’s political news that moves the markets. During the past week, for example, all kinds of prices have moved, sometimes by large amounts, in response to the mere utterances of the key actors in the geopolitical drama. The price of gold, the price of oil, the exchange rate of the ruble, the European and American stock markets, as well as a host of exchange-traded instruments linked to measures of volatility — all have gyrated as the world’s managers of money have adjusted their probabilities of war upward or downward.

Year-to-date prices demonstrate the uncertain effects of possible war in Ukraine

Source: Bloomberg

This interplay between political events and financial markets was the central preoccupation of my early work as an historian. Despite my best efforts, I continue to feel that most people who write history — especially of the modern era, since the advent of bond and stock markets — underestimate the importance of the “cash nexus”: the crucial interface between power and money.

This is probably because professional historians rarely have the funds (or the inclination) to engage in speculation themselves. (My boyhood hero, the great English diplomatic historian A.J.P. Taylor, was a financial dunce who fared disastrously in the 1970s inflation.) They also tend to study the emperors, the kings and queens, the presidents and prime ministers, rather than the bankers and brokers. Writing the histories of some of the great German-Jewish banking dynasties, the Rothschilds and the Warburgs, I learned to see history from a different vantage point.

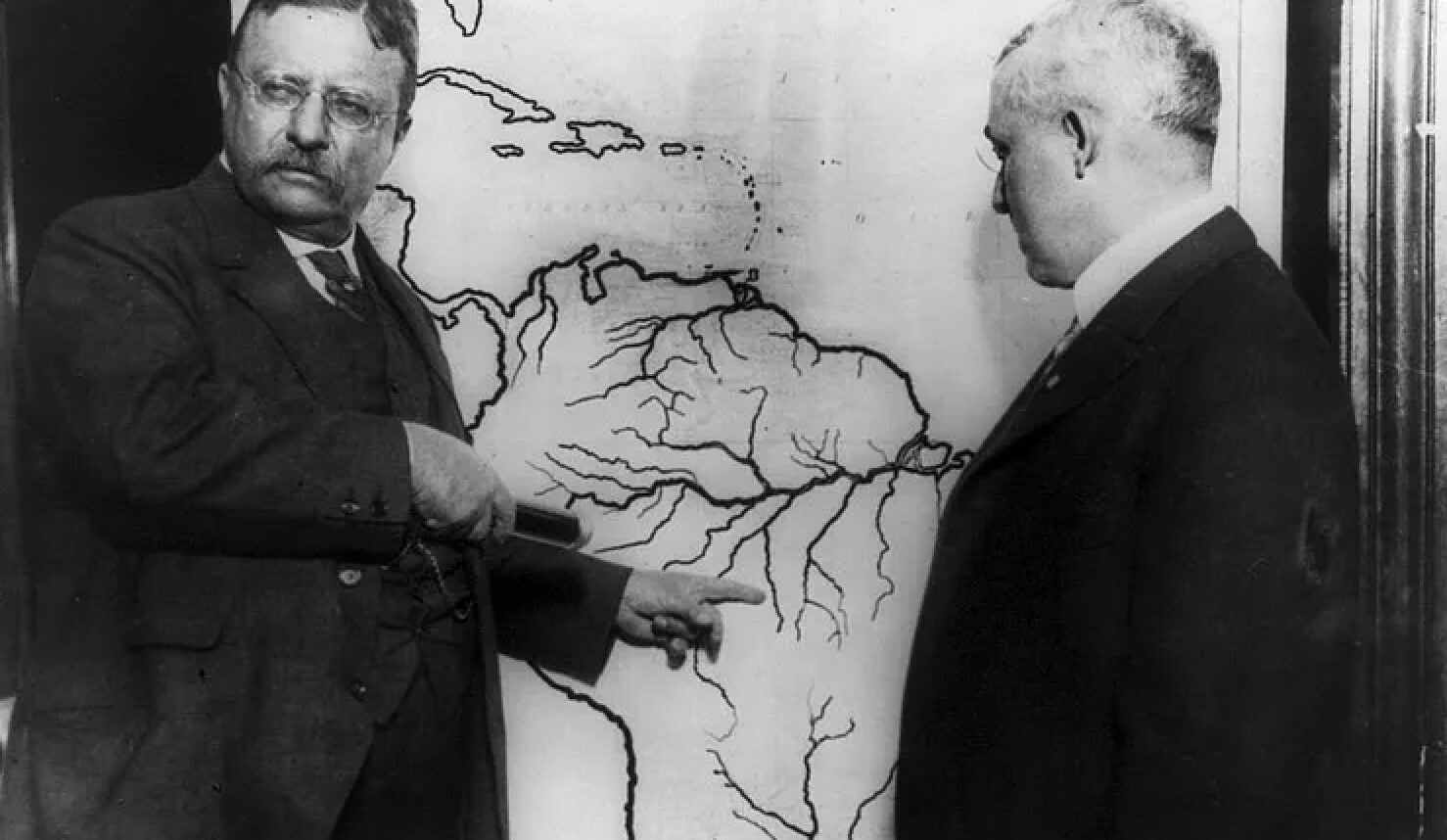

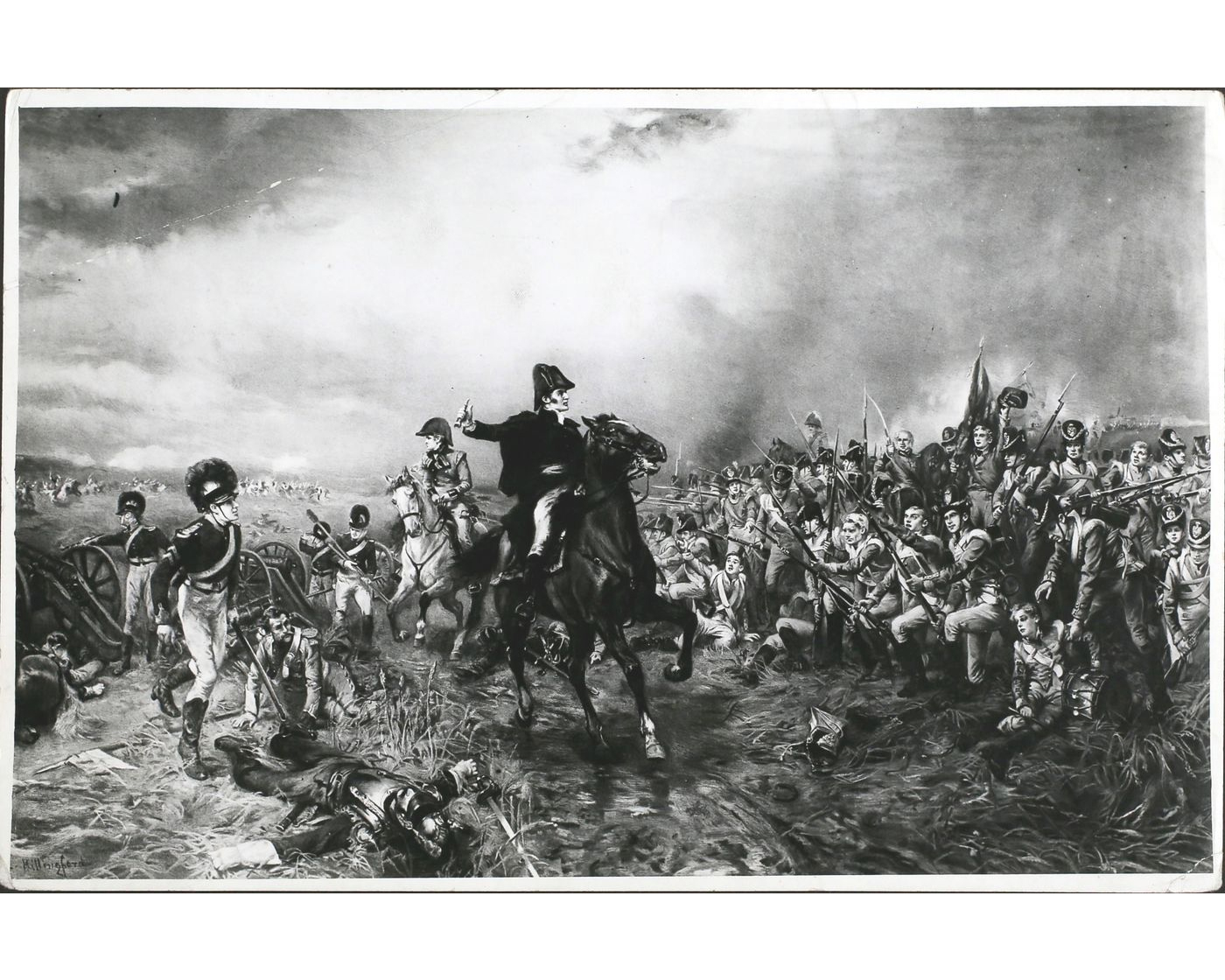

The story of how the Rothschild brothers profited from early news of the outcome of the Battle of Waterloo is the stuff of legend, including the toxic legend of Nazi propaganda. The reality is that Napoleon’s defeat, just 100 days after his return from exile on the island of Elba, was not at all what Nathan Rothschild had anticipated. He and his four brothers had built their father’s business from a modest coin dealership in the Frankfurt ghetto to an international trading house by seizing the opportunities presented by two revolutions: the British Industrial Revolution and the French political one. Nathan began exporting Lancashire cloth to the continent, but soon found there was more money to be made supplying Britain’s war effort with gold.

By the time of Napoleon’s initial defeat in 1814, the Rothschild brothers had learned two crucial lessons. Because of the economic disruption it caused, war tended to push up the price of gold in sterling terms because the gold-standard rule that allowed convertibility of pounds into gold at a fixed price had been suspended for the duration of the hostilities. Just as importantly, war drove up short- and long-term interest rates. The worse things went for Britain and her allies, the lower the price of “consols” — the near-perpetual bonds that the British government had been using to fund its large national debt since the mid-18th century — hence the higher the yield on those bonds. The worse things went for Napoleon, the lower the price, and hence the higher the yield, of rentes, the French equivalent of consols.

When Napoleon returned to France and reclaimed his imperial crown in March 1815, the Rothschilds assumed that another protracted period of conflict was beginning. They positioned themselves accordingly, acquiring gold wherever they could obtain it from their extensive credit network. They underestimated the effectiveness of the allied military response, which culminated in victory at Waterloo on June 18.

When the news of Bonaparte’s defeat reached the Rothschild offices in St Swithin’s Lane in London — delivered by a courier, not the carrier pigeon of legend — the brothers were therefore dismayed. If the war was over, the gold they had accumulated was not going to be needed and would indeed swiftly depreciate in terms of sterling. Nathan salvaged the situation with a spectacularly bold trade that amply justified his reputation as “the Napoleon of finance”: He bought consols on a massive scale and reaped a huge return as they rallied on the news of peace.

We now know that Napoleon’s final and irrevocable defeat at Waterloo ushered in a century of comparative peace in Europe. There was no major war involving all the great powers until World War I began in August 1914. But there were numerous smaller conflicts that might have escalated into a general war. And the Rothschilds, having made their fortune, had every incentive not to lose it again by being caught out in such a scenario.

As I came to see, poring over their extraordinary correspondence — the sometimes daily exchanges between London, Paris, Frankfurt, Vienna and Naples — the most important question the Rothschilds asked themselves was: Is the probability of another big war going up or down? Every scrap of news helped them to answer that question with greater precision and to position themselves accordingly. For example, they worried year after year that another French revolution might set in motion a repeat of the events of the 1790s, when a revolutionary regime had ended up at war with Europe for the better part of two decades. Revolutions in Paris in 1830, 1848 and 1871 set the alarm bells ringing, though history did not repeat itself.

There were of course a great many other things that the Rothschilds and their contemporaries had to worry about. Just as influential over the financial markets of the 19th century were the fluctuations of the business and credit cycle, which led to at least one significant panic in the City of London per decade. The ebbs and flows of liquidity were in turn connected to a variety of other phenomena, not least the vagaries of European harvests. In the mid-1840s, economic and political risk coincided and interacted. The harvest failures that drove food prices to spike in 1847 led directly to the political revolutions that swept the Continent, including France, the following year. For the Rothschilds, 1848 was the most terrifying year of the century — the moment they stared into an abyss as markets and governments tumbled.

Source: Bank of England

Note: Annual averages. Long-term bonds are consols from 1756

With the benefit of hindsight, we can see the period 1815 to 1914 as a period when economic and political risks declined while financial markets became broader, deeper and more resilient. Great forces were at work. The Industrial Revolution gathered speed and spread across the Atlantic and the Channel. The revolutionary ideas of 1789 and 1848 mutated to produce nonrevolutionary political movements — liberalism and social democracy — while conservatives learned to win elections.

Almost as significant, finance grew more stable. The gold standard spread, and panics in London grew less frequent. Joint-stock banking created bigger and better-capitalized financial institutions with larger and better-structured balance sheets. Savings institutions mobilized large amounts of capital from millions of small contributions. For all these reasons (described in more detail here), there was a tendency for financial markets to become less volatile and for the spreads between risky and safe investments to decline.

However, contemporaries tended not to be as aware of such long-term trends. The Rothschilds could not be sure the world had fundamentally changed since their formative years; nor could they know in advance that all the wars fought in Europe between Waterloo and 1914 would be relatively small and short. Just as we cannot be sure about whether war is coming to Ukraine, the Rothschilds could never be certain that Europe would avoid a major conflagration for a century.

In 1875, for example, German Chancellor Otto von Bismarck’s mouthpieces in the German press asked, “Is war in sight?” — unleashing panic on French markets. The alarm proved to be false; possibly Bismarck had never intended anything more than to beat the militarist drum for domestic political reasons.

To the Rothschilds, reassurance came from the news that their friend Benjamin Disraeli, the British prime minister, had set aside Anglo-Russian differences over Central Asia in the interests of preserving peace in Europe. “Last evening,” reported Charlotte de Rothschild to her son Lionel, “[Dizzy] paid a flying visit to your father, and told him of his immense success in negotiating for the maintenance of peace on the continent.”

The problem about prolonged periods of peace punctuated by small wars is that you get used to the quiet life. By the summer of 1914, even the Rothschilds — by now two or three generations away from the Frankfurt ghetto — struggled to imagine a world war. When the guns of August opened fire, they were caught out, along with most investors.

We have forgotten all about it now, but the financial crisis of 1914 — which began in July, before the war itself broke out — was the biggest in history, bigger even than the crisis of 1929. So severe was the liquidity crunch as the diplomatic situation deteriorated that trading on all the major stock markets of the world had to be suspended. The New York Stock Exchange remained closed from July 31, 1914, until Nov. 28 (when bond trading resumed) and Dec. 12 (when stocks could be bought and sold again). The Dow plunged 24.4% that day.

There was an almost complete contrast between the approach of war in 1914 and its approach in 1939. Markets were braced for war already in the summer of 1938. Although British Prime Minister Neville Chamberlain’s strategy of appeasing Adolf Hitler in Munich seemed to avert disaster, the more astute financial commentators (notably the Economist) appreciated that he had merely postponed it, and potentially given Hitler time to strengthen his position.

Our mindset today is more that of 1914 than that of 1938. For much of the period from 1945 until 1991, it is true, the world lived under the threat of a nuclear war between the U.S. and the Soviet Union. But the larger their arsenals of warheads became, the harder it grew to imagine such a war, even when it came close to happening over Cuba in 1962 and in the Able Archer false alarm of 1983. Instead of Armageddon, the Cold War saw a succession of proxy wars of varying sizes. The biggest were in Korea and Vietnam, but there were numerous smaller conflicts from Central America to southern Africa.

Markets mostly ignored both the threat of Armageddon and the proxy wars. After all, what kind of trade would pay off in the event of mutually assured destruction? By definition, it’s impossible to be short mankind, long apocalypse.

The biggest Cold War trade was to buy gold in anticipation of inflation. That paid off handsomely, especially after President Richard Nixon ended the Bretton Woods link between the dollar and gold. As inflation expectations surged in the late 1960s — and especially after the outbreak of the Yom Kippur War in October 1973 — being long gold was the winning move at a time when investors in bills, bonds and stocks were bleeding out. A second phase of geopolitical instability in 1979 — which saw the Islamic revolution in Iran and the Soviet invasion of Afghanistan — further rewarded the gold bugs. But that was the time to sell, with the price above $675 U.S. dollars per troy ounce, nearly 20 times higher than when Nixon was elected president in 1968.

A very precious metal in times of geopolitical risk

Source: Bloomberg

With Paul Volcker at the Fed, the great inflation came to an end, and with it the gold trade. As the Cold War ended in the late 1980s without a missile being fired, and the dot-com boom gathered steam, war risk faded from investors’ minds. The financial impacts of successive geopolitical events — the Gulf War, the wars in the Balkans, 9/11, the Afghan War, the Iraq War, the 2014 Ukraine crisis — were entirely overshadowed by the huge monetary expansions that followed the Lehman Brothers bankruptcy in 2008 and the Covid-19 pandemic.

If nothing else, Putin has reminded us that investors — even those bottom-up, value investors who protest that they couldn’t care less about either geopolitics or macroeconomics — can’t afford to ignore the unpredictable forces that lead to major wars. A Russian invasion of Ukraine would not be 1914 — not even close — as no one today is obliged to defend Ukraine the way Britain and France were bound to uphold Belgian neutrality. But a war in Ukraine would be a bigger deal than either the Afghan War or the Iraq War for two reasons.

First, even if everything went according to Putin’s plan and the Russians swiftly overran the Ukrainian military, the rest of Europe would be forced to face the return of Russia as a major power capable of threatening Ukraine’s neighbors and near-neighbors, too, rather than just a convenient source of natural gas, caviar and rubles in need of laundering.

Second, and more important, the economic and financial sanctions that the U.S. and its allies would then impose on Russia would significantly disrupt not only the Russian economy but that of each of Russia’s major trading partners, too. If the Russians imposed counter-sanctions, the disruption would be greater still. This scenario would imply some career-making wins for everyone who started the month short Russia’s currency, bonds and stocks and long gold, oil and gas and all those rarer commodities (e.g., titanium and palladium) that Russia exports. Only the parallel diplomatic effort to salvage the Iranian nuclear deal, which would bring Iranian oil back into the official global market, has put a lid on oil prices in the past week.

As an investor, you may not be interested in war, but war is interested in you. One in Eastern Europe would significantly complicate life for the world’s central bankers, who already have a problem on their hands, having so badly underestimated the inflationary consequences of the pandemic-induced fiscal and monetary measures of 2020-21. War would add to the inflationary pressures while at the same time tightening financial conditions and potentially hurting European business and consumer confidence.

But that’s not all. If Russia is successful in decisively ending Ukraine’s bid to become a Westward-looking democracy on a path toward European Union if not North Atlantic Treaty Organization membership, then China’s leaders may be tempted to conclude that they might get away with forcibly ending Taiwan’s autonomy and democracy. If they are right about that, we might find ourselves in a post-American world — a world in which China is No. 1 in the Indo-Pacific region and beyond — much sooner than most of us expected, with profound implications for the world’s readiness to regard dollars as the world’s reserve currency and U.S. government debt as the safest of financial assets.

But if the Chinese get that wrong — if the U.S. decided to honor its longstanding commitment to resist a non-peaceful change to Taiwan’s status — we might find ourselves in an even bigger war than anything currently being contemplated, with financial consequences that even Nathan Rothschild would have found daunting.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Dr. Scott Gottlieb on Finding Cures for Rare Diseases

Former FDA Commissioner Dr. Scott Gottlieb joins ‘Squawk Box’ to discuss the ongoing research and efforts at the FDA to find cures for rare diseases.…

Thought Leader: Scott Gottlieb

Peter Zeihan: U.S. Navy Seizes Russian Tanker

The US Navy just seized a shadow fleet tanker that managed to slip past the naval quarantine around Venezuela. The tanker reflagged as Russian while…

Thought Leader: Peter Zeihan

Erika Ayers Badan: Surviving Company Failure

In this episode of WORK: Unsolicited Advice, Erika talks through what it really looks like to come out of the worst month of your career…

Thought Leader: Erika Ayers Badan

Niall Ferguson on the Trump Corollary and Venezuela

Thought Leader: Niall Ferguson

Niall Ferguson: Global Conflicts to Watch in 2026

Thought Leader: Niall Ferguson