“My hope is that it creates world peace or helps create world peace.” That’s what Jack Dorsey, the former Twitter Inc. chief executive and now head of the digital payments company Block Inc., said about Bitcoin at a webinar in July 2021.

It is more likely that war creates a bigger global appetite for Bitcoin. Times of tumult are often associated with monetary transformations. A classic example is the way, in the time of the Black Death and the Hundred Years’ War, the English monetary system was fundamentally altered.

There was a post-plague spike in commodity prices — especially for salt, the price of which rose sevenfold from 1347 to 1352. At the same time, the survivors of the Black Death were able to exploit a tight labor market to exchange feudal bondage for cash wages. The English economy became increasingly monetized.

European merchants, meanwhile, developed a new form of peer-to-peer credit instrument, the bill of exchange, which facilitated trade between England, the Low Countries and northern Italy.

More recent examples abound. The Spanish conquests in the New World transformed the global economy by increasing the supply of silver and gold, much of it used to pay for the Habsburgs’ European wars. The expansion of the British Empire exported the gold standard, creating a new and more stable international monetary system in which sterling was the dominant currency. The world wars left Britain weighed down by debt and ushered in the first era of dollar dominance, with the U.S. currency pegged to gold and all the other major currencies less rigidly pegged to the dollar.

It was conflict, once again, that ended that Bretton Woods system in 1971. As the Vietnam War dragged on, President Richard Nixon’s breaking of the dollar’s peg to gold ushered in a new era of floating fiat currencies, characterized at first by high inflation and exchange rate volatility, then by a series of international agreements (the Plaza Accord in 1985, the Louvre Accord two years later), latterly by more ad hoc and less transparent arrangements in an environment of falling inflation and rapidly growing capital flows.

The events of the past two years — first the Covid-19 pandemic and now the Russian invasion of Ukraine — have been sufficiently disruptive to make another shift in the global monetary order seem likely. But what form will it take? Two hypotheses have come to the fore, by no means mutually exclusive.

The first is that cryptocurrency’s hour has arrived. In the words of Michelle Ritter, chief executive of the tech company Steel Perlot Management LLC, “Social media’s hinge moment came in 2011, when videos, tweets and other posts from Libya, Egypt, Yemen, Syria and Bahrain sparked the Arab spring … [Now] we find ourselves at a similar turning point” with cryptocurrency. The hedge fund Bridgewater Associates LP noted that “Russia’s invasion of Ukraine is the first major event where cryptocurrencies are part of the equation.”

Hypothesis two is that we are witnessing the twilight of the dollar. According to Zoltan Pozsar of Credit Suisse Group AG, the decision by the U.S. and its European allies to freeze much of the Russian central bank’s foreign-exchange reserves was a watershed moment. It will, he has argued, “encourage central banks to diversify away from the dollar, or try to re-anchor their currencies to assets that are less susceptible to influence from U.S. or European governments.”

According to Pozsar’s March 7 note, “Bretton Woods III,” we are leaving behind the post-1971 Bretton Woods II, a system in which “inside money” (U.S. Treasuries) replaced “outside money” (gold). Bretton Woods III will take us back to outside money (gold and other commodities) as the world reduces its reliance on dollars and dollar-denominated bonds.

BitMEX founder Arthur Hayes made a similar point in his March 16 essay, “Energy Cancelled.” “Why should any central bank ‘save’ in any Western fiat currency, when their savings can be expropriated arbitrarily and unilaterally by the operators of the digital fiat monetary networks?” In “The Doom Loop,” he predicts “$1 million Bitcoin and $10,000–$20,000 gold by the end of the decade.”

These gentlemen are by no means the first to predict the demise of the dollar. But whenever I hear such arguments I am reminded of an old Larry Summers line. Speaking at Harvard’s Kennedy School of Government in November 2019, the former Treasury secretary observed: “You cannot replace something with nothing.” What other currency was preferable to the dollar as a reserve and trade currency, he asked, “when Europe’s a museum, Japan’s a nursing home, China’s a jail, and Bitcoin’s an experiment”?

First, take a look at what happened when crypto went to war. At the beginning of the Russian invasion there was a great deal of discussion about how the Kremlin would somehow use cryptocurrency to evade Western sanctions. Certainly, there was an initial surge of ruble purchases of Bitcoin.

But American and European regulators put the major crypto exchanges on notice. Coinbase Global Inc. blocked over 25,000 Russia-linked addresses that it believed were linked to illicit activity. In any case, as Tigran Gambaryan of Binance Holdings Ltd. pointed out, “Crypto is not a very efficient way for a government and for a nation-state to elude sanctions.”

Crypto played a bigger part in facilitating private donations to the Ukrainian government. According to Gillian Tett of the Financial Times, writing on March 10, “about $106 million of crypto donations have flooded in.” Vitalik Buterin, the founder of Ethereum, tweeted: “Reminder: Ethereum is neutral, but I am not.” His co-founder, Gavin Wood said he would “personally contribute $5 million” if Polkadot, his new token, was accepted. Sergey Vasylchuk, chief executive of blockchain company Everstake, launched a decentralized autonomous organization based on the Solana blockchain to raise donations for the Ukrainian army.

Slava Ukraini!But please note that $106 million is a rounding error compared with the amounts of dollar-denominated military aid Ukraine is receiving from the U.S. government, which could total $19.67 billion if the Biden administration’s latest proposal is approved by Congress.

Let’s keep this simple. Cryptocurrencies such as Bitcoin and Ethereum are attractive assets to hold in unstable places and at unstable times. Certain kinds of stablecoins (pegged to the U.S. dollar) may be even more attractive. As Sirio Aramonte, Wenqian Huang and Andreas Schrimpf point out in a recent Bank for International Settlements note, that’s why there was so much Turkish trading in stablecoins in 2020 and 2021, as the pandemic combined with the Turkish government’s reckless monetary policy to tank the lira.

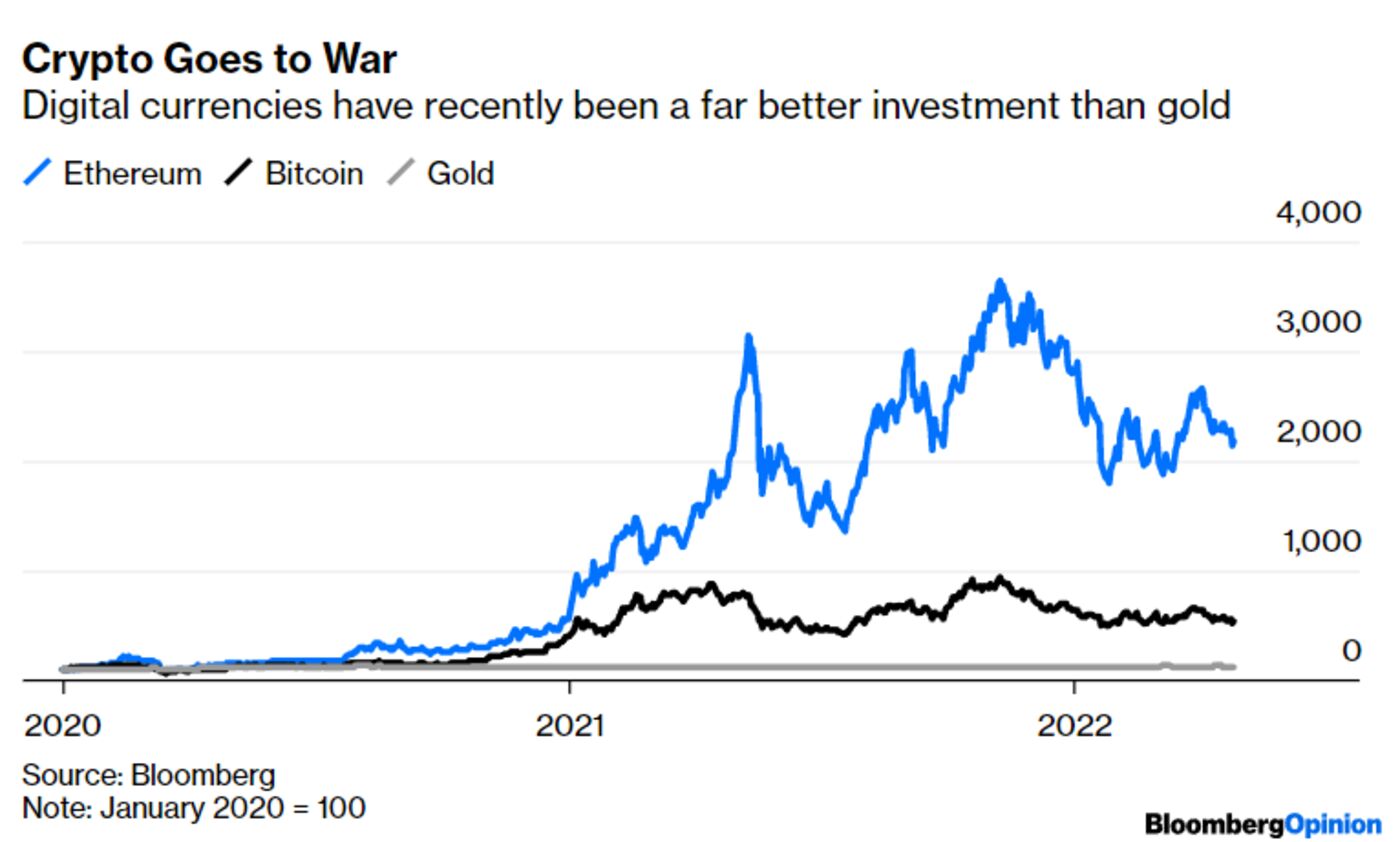

When the pandemic began, you really were well advised to put some money into Bitcoin and Ethereum. Relative to January 2020, your investments are up by factors of, respectively, 21.7 and 5.4. Your gold position is up just 25%. Even in time of war, crypto has beaten out gold. Since the eve of the Russian invasion, Bitcoin is up 3.8%, Ethereum 9.1% and gold is down 1%.

But in war one needs more than assets that retain or gain value. It is much more important to be able to make payments to domestic and foreign vendors in return for the stuff you need from them. As is well known, the Ethereum blockchain can process only about 15 transactions a second, whereas Visa can handle thousands of credit-card transactions a second.

For Russia over the past two months, it was more important that Western credit-card companies could not disable Russian payments than that Russians could buy Bitcoin. And that is because since 2014 (when their first, more limited invasion of Ukraine happened) the Russians have built their own National Card Payment System (NSPK) for processing transactions and a domestic card system known as Mir which runs on the NSPK rails — as do cards issued by China’s UnionPay Co.

In the great scheme of the global economy, digital payments are a bigger deal than crypto. That is because payments systems exploiting artificial intelligence — such as Ant Financial Services Co.’s Alipay and Tencent Holding Ltd.’s WeChat Pay — can process vastly more transactions much faster than any blockchain-based system and can then spit out credit ratings based on the data they aggregate and analyze.

Several years ago, I grew very concerned that these Chinese payment systems were going to eat the world — or at least were going to become dominant in emerging markets. Fortunately for the Western world, the Chinese Communist Party decided that Alibaba founder Jack Ma was getting too big for his boots and pulled the plug on his and Eric Jing’s plans for world domination.

The Chinese challenge in payments is not over, however. Bytedance Inc.’s immensely popular TikTok platform is implementing payments features. Kenyan fintech giant M-Pesa, Ethiopian state-owned Ethio Telecom and Pakistani telecom provider Jazz are among the companies in 19 countries using Huawei Technology Co.’s Mobile Money platform. Chinese-owned African mobile payments platform OPay is now the second-largest fintech startup in Africa in terms of size and value.

But the new thrust of Chinese policy is to persuade other countries’ central banks to develop digital currencies that are interoperable with China’s central bank digital currency, e-CNY, via “bridges” between central banks. Thailand, Hong Kong and the United Arab Emirates are working with China on such bridges. China’s alternative to SWIFT — a renminbi-denominated Cross-border Interbank Payments System — now has 1,200 member institutions across 100 countries.

Another Chinese agency is the state-backed Blockchain-based Service Network (BSN), which aims to create a digital architecture connecting public and private blockchains. In 2021, BSN launched the Universal Digital Payment Network, which seeks to build a “standardized digital currency transfer method and payment procedure.”

According to Chinese reports last August, at least three foreign banks are planning to access e-CNY through a private clearing platform built by Shanghai’s City Bank. As the February 2022 Beijing Olympics showcased, foreigners in China can already create their own e-CNY wallets without a Chinese banking account.

Yet if China plans to build an alternative payments architecture to the one dominated by American and European institutions, it has a very, very long way to go. In January, shortly before the Russian invasion of Ukraine, China held just over $1 trillion of its roughly $3 trillion worth of foreign reserves in U.S. Treasury bonds, according to the Treasury Department. More than half of China’s reserves are denominated in dollars, according to the most recent data published by the State Administration of Foreign Exchange.

Beijing has clearly been flabbergasted by the U.S. decision to freeze Russia’s central bank reserves. “Chinese economists … find it shocking that the U.S. would carry out such measures against Russia,” wrote the Chinese economist Yu Yongding of the Chinese Academy of Social Sciences last month. “The international financial system is based on the trust that all participants will play by the rules, and honoring debt obligations is one of the most important rules there is. Whatever the justification, freezing a country’s foreign-exchange reserves is a blatant breach of that trust … Now that the U.S. has proved its willingness to stop playing by the rules, what can China do to safeguard its foreign assets? I don’t know.”

I don’t know either. The problem for China is that prophecies of the dollar’s demise, which people have been making since the late 1960s, keep turning out to be wrong. True, as the University of California, Berkeley’s Barry Eichengreen has pointed out, the dollar’s share of allocated international reserves has declined somewhat since the beginning of the century, from 71% to 59%. But it’s not as if central banks have been swapping dollars for renminbi.

The currencies that have grown more popular with reserve managers are those of Canada, Australia, Sweden, South Korea and Singapore. This is not an erosion of dollar dominance that greatly diminishes the ability of the U.S. to impose financial sanctions. As the Russians have discovered, even the Swiss were willing to participate in the Russian reserve freeze.

Still Stockpiling Dollars

Total foreign exchange reserves

Source: International Monetary Fund

Nor is that the only measure of dollar dominance. In 2021, the U.S. currency was used in 40% of all international payments by total transaction value. In second place was the euro. The Chinese currency came a miserable fourth — just 2.7% — behind even sterling.

The West Is Winning on SWIFT

Most active currencies for international payments in 2021

Source: Society for Worldwide Interbank Financial Telecommunication

In the words of Sebastian Mallaby of the Council on Foreign Relations:

Dollar defeatism is vastly overblown. Around the world, almost three-fifths of private foreign-currency bank deposits are held in dollars. A similar share of foreign-currency corporate borrowing is done in dollars. … The Federal Reserve estimates that foreigners hoard about half the outstanding stock of dollar bank notes. … [Foreign central banks] hold dollars knowing that others will gladly accept them, just as many learn English because others speak it. … A standing credit line in renminbi is the financial equivalent of fluency in Esperanto.

As the prolific economic historian Adam Tooze points out, the other central banks that issue reserve currencies are all on the other end of swap lines from the Federal Reserve, key sources of liquidity in times of financial crisis such as late 2008 and early 2020. Meyrick Chapman argues persuasively that, for the global economy, “America remains the ‘consumer of last resort.’ Until that changes, the dollar will retain its ascendency.”

All of this helps explain the extraordinary dollar rally we have seen this year, which has seen it strengthen significantly against most other major currencies, particularly the Japanese yen, which has depreciated by nearly 27% since the beginning of 2021. The euro is down by 16%, the pound by 10%.

An Extraordinary Rally

Dollar exchange rates with global currencies

Source: Bloomberg

Note: January 2020 = 100

Can we therefore, like Larry Summers, dismiss cryptocurrency as a mere experiment? Some might go even further, condemning it as no better than a host of Ponzi schemes. There are now between 10,000 and 20,000 different cryptocurrencies in existence, according to CoinMarketCap. That would be excessive even if they were all impeccably designed and managed.

There is a great deal of loose talk among the crypto bros. What is one to think when (for example) Mike Novogratz of Galaxy Digital LP says of his favorite stablecoin, Terraform Labs’ UST, that it’s “all good as long as there’s not a run on the bank.” What, like Lehman Brothers?

Or how about this from Sam Bankman-Fried, founder of crypto exchange FTX, who was asked to explain the practice of yield-farming on Bloomberg’s “Odd Lots” podcast. Yield farming, to put it simply, is borrowing someone else’s crypto tokens in exchange for your own “governance tokens,” and then exchanging the borrowed tokens for higher-yielding DeFi (decentralized finance) instruments. This was how Bankman-Fried put it:

Like this is a valuable box as demonstrated by all the money that people have apparently decided should be in the box. And who are we to say that they’re wrong about that? … And so then, you know, [the governance] token price goes way up. And now it’s a $130 million market cap token because of, you know, the bullishness of people’s usage of the box. And now all of a sudden, of course, the smart money [goes and pours] another $300 million in the box and … it goes to infinity. And then everyone makes money.

Never mind the Wild West; this is the Wacko West. According to a report from the blockchain analytics firm Elliptic, around $10 billion in DeFi projects was lost to various hacks and scams in 2021. In one case, members of the Bored Ape Yacht Club — who collect non-fungible token cartoons of, yes, bored apes — were duped into giving up the passwords to their crypto wallets.

When you read such stories, you begin to understand the strong impulse of so many central bankers and financial regulators around the world to shut down the whole crypto circus. Some countries have already banned the use of crypto for payments as well as bitcoin mining: not only China, but also Algeria, Bangladesh, Bolivia, Egypt, Morocco and Nepal.

There are European and American officials who itch to regulate crypto more tightly, if not to ban it, such as Fabio Panetta of the European Central Bank, Gary Gensler of the Securities Exchange Commission and acting U.S. Comptroller of the Currency Michael Hsu, who recently compared the current state of crypto to the “fool’s gold rush” before the 2008-9 financial crisis.

We know already which way Brussels will go. Grinding its way through the European bureaucracy is the European Commission’s Markets in Crypto-Assets Regulation, which will require crypto exchanges to make full disclosure of everyone buying and selling digital assets. The British government, by contrast, clearly hopes to attract more crypto business to London — hence Chancellor of the Exchequer Rishi Sunak’s suggestion that the venerable Royal Mint should develop an NFT, a flight of fancy that went down badly with Patrick Jenkins of the Financial Times(“the crypto cult exudes an oligarch-like arrogance”).

But what will the U.S. opt to do? Last year it seemed as if the Genslerites were in the ascendant and European-style regulation was only a matter of time. All that changed with the fight that broke out inside the Beltway over last year’s infrastructure bill, which alerted a significant number of Democratic legislators to the fact that the U.S. crypto community now has both votes and dollars.

According to a recent Morning Consult survey, 20% of American adults and 36% of millennials own cryptocurrency. As Kevin Roose pointed out in a voluminous primer for the New York Times, crypto is suddenly ubiquitous, with Matt Damon and Larry David doing ads, the mayors of Miami and New York City touting their pro-bitcoin credentials, Colorado and Florida vying to be the No. 1 crypto state, two NBA arenas named after crypto companies, and both Pepsi and Applebee’s offering their own NFTs. Most important of all, “crypto entrepreneurs are donating millions of dollars to candidates and causes, and lobbying firms have fanned out across the country to win support for pro-crypto legislation.”

The first fruit of all this lobbying was the White House executive order issued on March 8, 2022, on the “Responsible Development of Digital Assets.”

Gone was the hostile language of last year. “The rise in digital assets creates an opportunity to reinforce American leadership in the global financial system and at the technological frontier,” states the EO. “The United States must maintain technological leadership in this rapidly growing space, supporting innovation while mitigating the risks for consumers, businesses, the broader financial system and the climate.”

This is crypto’s glad confident morning in Washington. “We are in a similar moment with cryptocurrencies,” declared Democratic Senator Ron Wyden recently, “to the one we were in 30 years ago in the early days of the Internet.” I hear this a lot in Silicon Valley, too. But what exactly does it mean?

It is generally agreed that the U.S. dominance of the first two eras of the Internet — Web 1.0 (nerds with email and web pages) and Web 2.0 (nerds making money by building platforms) — owed much to the relatively permissive legislation passed by Congress in the 1990s, notably the 1996 Communications Decency Act, and specifically its Section 230.

In essence, Section 230 created a special regulatory space for the rapid development of Internet platforms by exempting them from the legal liabilities associated with publishing companies, while also entitling them to moderate content as they saw fit. The really interesting question for today’s legislators is: What would a Section 230 for DeFi/Web 3.0 look like? In a provocative new blog post, Manny Rincon Cruz proposes three elements:

No Virtual Asset Service Provider (VASP) status for developers of decentralized protocols. Code is already protected as free speech, and decentralized protocols have no intermediaries providing exchange, custody, or transfer services because DeFi users transact directly with each other.

Exclude DeFi “exploits” from the Computer Fraud and Abuse Act (CFAA). Exploits occur when a user interacts with a protocol, as its code is written, and profits by taking advantage of arbitrage opportunities or design weaknesses. As long as users do not break other criminal laws, exploits help DeFi by exposing buggy code.

No banking charter requirements for stablecoin issuers such as Circle and Tether. Unlike bank deposits, users can sell their USDC or USDT without redeeming them. Since these stablecoins cannot produce “bank runs,” they should not be subject to banking-specific regulations.

No doubt this is just the beginning of a debate about what light-touch regulation might look like for Web 3.0. But it is surely a better debate to have than one about how to out-regulate the Europeans. The point is that U.S. dollar dominance and flourishing crypto are not alternatives to one another, but complementary. Just as Bitcoin was never meant to be — and never will be — a substitute for the dollar, so DeFi is additional to rather than a substitute for the existing financial system, which we shall no doubt continue to use for decades to come in order to pay our taxes and also, I would guess, our employees and our utility bills.

Bitcoin is not about to bring about world peace, despite the hopes of some early enthusiasts. Nor will crypto emancipate us from the protective if sometimes stifling embrace of the nation-state, as some radical libertarians once imagined. But if decentralized finance becomes as big an American success story as e-commerce has been, then it will provide yet another reason for foreigners to invest in America — and therefore to own and transact in dear old dollars.

The holidays are full of stories, laughter, and maybe a little disagreement. Ever try telling a story and hear someone say, “That’s not what happened!”? There’s actually science behind it. Dr. Signy…

Dr. Elizabeth Economy sits down with Patrick McGee to discuss how Apple’s deep integration into China’s manufacturing ecosystem inadvertently helped build China into the industrial…